The geopolitics of compute: why big tech is moving the AI stack to India

1. Introduction: the groundbreaking in Tarluvada

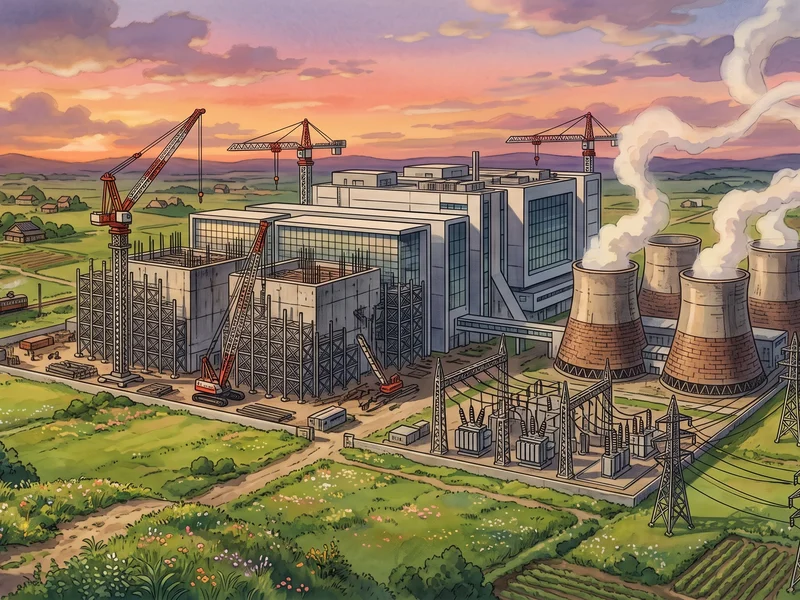

On April 28, 2026, in a quiet village called Tarluvada, about 30 kilometers from the coastal city of Visakhapatnam, the physical center of gravity of global tech power shifted a little. Among mango groves and paddy fields, a group of hyperscalers led by Google poured the first concrete for a data center campus built specifically for AI workloads. The number attached to phase one alone: $15 billion over five years, making it one of the largest dedicated AI compute hubs outside the United States.

This isn’t happening in the places you’d expect, not Tokyo, not Frankfurt, not Singapore. It’s happening on thousands of acres of rural Indian farmland.

Rough shape of the deal: US and EU power grids are maxed out and running into local protests, India is offering a 21 year corporate tax holiday, and the initial 1 GW of capacity (with room to scale to 5 GW) puts these companies within a direct line to 700 million multilingual users.

To actually understand this shift, you need to get past the clean corporate marketing and look at what’s really going on underneath it. This is a real reworking of the global compute supply chain, driven by resource scarcity in western markets and pulled along by long-term tax incentives, with the world’s biggest tech firms anchoring the physical guts of AI in the Global South.

Which brings up the real question here: is this infrastructure boom the thing that pushes India toward the top of high-value software engineering, or is it the setup for a new kind of digital extraction economy?

2. The scale of the Indian infrastructure boom

The physical size of the Visakhapatnam project doesn’t really match how we normally think about data center scaling. Phase one alone is built for 1 gigawatt (GW) of continuous, active power draw, and the land reserved is meant to eventually support up to 5 GW.

To put that in context, here’s how it stacks up against what India has already built:

| Metric | India’s national footprint, 2000 to 2025 | Visakhapatnam, phase 1 | Planned ceiling |

|---|---|---|---|

| Power capacity | ~1.5 GW total, combined across all major metros | 1.0 GW allocated | 5.0 GW at peak |

| Land footprint | Scattered urban warehouse spaces | 600 acres, one contiguous industrial zone | 2,000+ acres regional reserve |

| Primary use | Traditional consumer web traffic | Deep learning training | Real-time model inference |

Sit with those numbers for a second. Over twenty five years of digital growth across Mumbai, Chennai, Bengaluru and Hyderabad, India built a combined national data center footprint of roughly 1.5 GW. One facility in rural Andhra Pradesh is going to match that entire historical footprint on day one, and eventually triple it.

And this isn’t a one-off. Microsoft is putting in $17.5 billion for cloud infrastructure across the Deccan plateau near Hyderabad. Amazon Web Services has committed $13 billion to expand operations in Maharashtra by 2030. Meta is locking down regional infrastructure partnerships of its own to anchor local services.

Zoom out further and hyperscalers globally are projected to hit $725 billion in capital expenditure in 2026 alone. That capital isn’t going into software optimization anymore. It’s turning into steel, high voltage transformers, and industrial concrete.

3. Why virtual systems need real ground

The common mental model people have of AI is wrong. We think of it as something ephemeral, decentralized, floating in “the cloud,” independent of physical constraints. In reality it’s one of the more resource-intensive industrial processes running right now.

Here’s roughly what happens, physically, every time someone sends a prompt to a large language model. It leaves a phone over wifi or cellular, hits a local router, travels through copper and then subterranean fiber optic cable, sometimes gets routed through a regional aggregation hub, sometimes crosses an ocean through subsea cable and lands at a continental station, and finally arrives at a hyperscale facility. Inside that facility, the actual computation runs on specialized chips that individually can cost more than a luxury car.

All of that processing generates heat, a huge amount of it. Managing that heat requires industrial-grade cooling, and at this scale that usually means evaporative cooling loops pulling millions of gallons of groundwater a day and turning it into steam.

So there’s a direct trade-off buried in every “instant” AI response: every bit of digital convenience is quietly backed by a real extraction of physical resources from the ground underneath the facility running it.

4. The supply chain pivot: domestic friction and geopolitical moats

The sudden migration of AI infrastructure toward corridors like India is really a response to growing constraints inside western domestic markets. In the US and parts of western Europe, hyperscale development is running into real trouble from energy limits and community pushback.

Local governments and activist groups have blocked or delayed at least 48 major data center projects, freezing roughly $156 billion in planned capital. Two things are driving most of that friction:

Grid stability is the first one. High-density server farms put a massive, continuous load on regional power grids, and utilities often end up keeping older fossil fuel plants running just to cover the base demand, which directly undercuts local emissions targets.

Water scarcity is the second. In regions already dealing with drought, pulling millions of gallons of water out of public aquifers to cool server racks creates real tension with agriculture and local communities who depend on the same water table.

On the other side of this, India’s policy environment is actively pulling that capital in. The Union Budget introduced a corporate tax holiday running all the way to 2047, twenty one years, for foreign companies deploying cloud services through Indian data centers. That’s an unusually long window of regulatory certainty for a foreign firm to plan around.

There’s a geopolitical layer to this too. As western countries tighten export controls on advanced AI models and specialized hardware (access to models like Claude Mythos 5 and Fable 5 was briefly suspended in mid-2026 under US export rules, for example), companies have a real incentive to anchor compute capacity in jurisdictions that sit further from that kind of sudden policy risk. Building large facilities directly inside India gives these companies operational hubs that are more insulated from abrupt shifts in western domestic policy.

5. The compute stack, layer by layer

To actually judge whether this infrastructure boom is good for India long term, you have to look at how value gets split across the different layers of the modern AI stack. It works as a rough vertical hierarchy, and the capital, the margins, and the actual value capture are spread very unevenly across four layers.

Layer one: foundational IP. This is the top of the stack, the model weights, the proprietary architectures, the training methods coming out of leading research labs. It’s highly scalable, needs almost no physical overhead to distribute, and captures the majority of long-term software margins, something in the range of 70 percent based on current US company economics. Ownership of this layer stays almost entirely inside western corporate labs.

Layer two: silicon. This is the hardware layer, specialized chips built for deep learning workloads. It’s dominated right now by concentrated players, Nvidia alone holds something like a 92 percent share of the data center accelerator market. This layer has serious pricing power, letting chip designers capture high margins on the silicon that everything else depends on.

Layer three: data center housing. This is the physical facility itself, concrete structures, power substations, automated cooling, server racks. It’s an asset-heavy, utility-style business: huge upfront construction costs, long depreciation cycles, and comparatively thin margins. This is exactly the layer where India is currently pulling in foreign capital.

Layer four: raw resources. The actual foundation underneath everything, industrial land, grid connections, a steady supply of water. This layer is a pure commodity business, and it’s the layer that carries almost all of the local environmental cost of the compute running above it.

Right now, India is capturing layer three. Everything about India’s long-term position in the AI economy depends on whether it can climb into layers one and two, or whether it stays permanently anchored at the bottom.

6. The Foxconn playbook, and where it breaks

The way global tech capital is flowing into Indian infrastructure right now closely mirrors a supply chain shift from twenty years ago: Apple’s move of its manufacturing base to China back in 2003.

Apple, at the time, was low on cash and facing flat growth. To stabilize the business, it made a strategic pivot that ended up reshaping global electronics manufacturing entirely, moving its assembly and supply network into specialized factories around Shenzhen.

Back then, most western analysts figured China would stay a low-cost assembly hub forever, permanently stuck at the bottom of the value chain. The early numbers seemed to back that read up: Apple kept roughly $320 in gross margin on every device sold, while a local assembly partner like Foxconn got about $8 per unit, plus all the localized labor and environmental overhead.

What those analysts missed was a slower, deeper trend: knowledge spillover is fluid once you put enough people through the same process for long enough. Over two decades of manufacturing devices for global brands, local engineers, component suppliers, and production managers ended up mastering the entire logistics chain of high-precision electronics manufacturing.

That accumulated expertise eventually broke out of the foreign corporate silos it started in. The local manufacturing ecosystem moved from simply assembling foreign components to designing and launching real, competitive domestic tech brands, Huawei, Xiaomi, BYD. That’s a genuine shift from low-margin assembly into high-value intellectual property, and it changed the shape of the entire regional economy.

That’s the optimistic version of what could happen in India. Here’s where the comparison actually breaks down: data centers do not require large amounts of human labor.

An electronics assembly plant needs thousands of technicians working directly with complex physical components, which naturally creates an environment where operational knowledge spreads to the local workforce whether the foreign company wants it to or not. A hyperscale AI data center is the opposite, a highly automated, capital-intensive facility that needs very little on-site human management once it’s built. A small team of facilities engineers can run the power infrastructure and cooling loops for an entire campus on their own.

And the actual high-value part of the system, the model weights, the optimization algorithms, the foundational logic cores, is never accessible to local teams at all. It runs as compiled software deep inside closed server networks, controlled from corporate headquarters somewhere overseas. What the local workforce ends up managing is the physical shell: pouring concrete, running high voltage lines, keeping water pumps working.

7. The risk of a digital extraction economy

This creates a real structural risk. If India doesn’t use this infrastructure boom to actively build domestic foundation models and its own chip design capability, it risks sliding into a pure digital extraction model, one where the country supplies the heavy physical inputs, regional electricity, groundwater reserves, industrial land, while the actual high-value intellectual property and long-term software margins keep flowing back to corporate hubs overseas.

That outcome isn’t locked in. It depends entirely on whether policy treats this construction wave as an end in itself, or as leverage to build something India actually owns.

8. Conclusion: the human cost of hyper-accelerated networks

There’s a strange contradiction sitting underneath all of this. As we build increasingly advanced software models, complex cloud networks, and deep learning systems, the entire infrastructure holding it up still comes down to one basic industrial process: burning resources to boil water and spin magnets.

Whether it’s a coal-fired grid or a nuclear-adjacent cooling loop, the virtual internet stays tethered to real, physical resource extraction.

This shift changes the relationship between the people who use technology and the companies who provide it. The Global South isn’t just a consumer market for digital apps anymore, it’s becoming the primary source of the raw materials, land, energy, water, data, that keep the global compute engine running.

As developers, policymakers, and everyday users deal with this shift, it’s worth looking past the clean software interfaces and actually confronting the physical footprint underneath our digital systems. Whether this infrastructure boom ends up being good for India comes down to one thing: can local industry climb the value chain and build sovereign technology, or will it mostly end up carrying the physical cost of somebody else’s centralized network.

Key takeaways

Google’s $15 billion investment in a 1 GW (scaling to 5 GW) facility in Visakhapatnam is, by itself, several times larger than India’s entire pre-existing national data center footprint. That’s a major geographic shift in where global compute infrastructure actually lives.

AI is a genuinely resource-heavy industrial process. Every automated interaction depends on deep-sea cable routes, high voltage transformers, and millions of gallons of water consumed for cooling.

The pivot toward markets like India is being driven by real constraints in the west, energy limits, grid caps, and environmental pushback that’s currently frozen around $156 billion in data center development.

The compute stack is deeply unequal. Foundational IP and chip design capture most of the market margin, while local hosting hubs mostly manage low-margin real estate and resource overhead.

Unlike labor-intensive electronics assembly, highly automated data centers offer much less room for local knowledge spillover, which creates a real structural risk of India ending up in a digital extraction economy if policy doesn’t push back on it.

FAQ

Why are global tech firms moving their major AI data centers to India? Tech firms are reallocating compute infrastructure because of a combination of western grid limits, rising water shortages, and real local pushback against server farm expansion in traditional markets. India offsets those constraints by offering large tracts of industrial land, a big pipeline of technical talent, and a 21 year corporate tax holiday running to 2047.

How much water and power do hyperscale AI data centers actually use? A standard hyperscale AI campus needs hundreds of megawatts of continuous power, sometimes scaling into full gigawatt loads for the largest training clusters. To keep that dense hardware from overheating, evaporative cooling loops consume millions of gallons of groundwater daily, which competes directly with local municipal and agricultural use.

What’s the actual difference between a data center hub and a foundational AI model? A data center hub is the physical infrastructure, real estate, server racks, electrical substations, cooling towers. A foundational model is the software IP, the core algorithmic weights, logic layers, and proprietary code running on top of that hardware. The physical data center captures utility-style rent. The foundational model captures the bulk of the software margin.

Can India replicate China’s manufacturing success through this data center boom? The path here is structurally different. Electronics assembly plants are labor-intensive and naturally spread technical skill across a large local workforce. Automated data centers run on centralized, closed server networks that need very little on-site human management once they’re built, which sharply limits organic local knowledge spillover.

What can local policymakers actually do to avoid a digital extraction scenario? Structure infrastructure approvals so they require parallel investment in domestic technology, funding for local AI research, domestic foundation models built for regional languages, and support for local semiconductor fabrication and chip design so India has a real shot at capturing high-value IP instead of just hosting someone else’s.

Comments

Related Articles

Never miss an update

Join 50,000+ developers getting our weekly tech insights.